L17 Insurance — Costs and What You Need to Know

Which insurers accept 17-year-old drivers, liability insurance costs, and what happens in an accident. Tips to save on L17 insurance.

Passing the exam and getting your license is one thing. Sitting behind the wheel of a car that's properly insured is another. And this is where many families make a mistake — they either ignore insurance entirely or get it wrong. The result? After your first minor accident, you discover that your parent's no-claims bonus they've built up for ten years is gone, or that comprehensive insurance doesn't cover damage to the car.

This chapter explains how insurance actually works under the L17 program, what you need to discuss with your insurer, how much it will cost, and what happens if you have an accident. We'll also walk through the dilemma every family faces: insure the car under the parent, or start building your own no-claims bonus from age seventeen?

Quick summary:

- Liability insurance belongs to the vehicle operator — if you drive your parents' car, you're automatically covered by their policy

- Five insurers accept 17-year-olds as independent policyholders: Allianz, Generali ČP, Kooperativa, ČSOB, Pillow

- Generali offers a 30% discount for L17 graduates with documented mentor rides

- Liability insurance for young drivers costs roughly CZK 5,100–25,000/year — depending on the car, location, and insurer

How insurance works under L17

Let's be straightforward: most L17 drivers don't drive their own car. You drive your mum's, dad's, or mentor's car. And this is the key piece of information, because since April 2024, the new liability insurance law (Act No. 30/2024 Coll.) says that insurance must be taken out by the vehicle operator — the person listed in the vehicle registration certificate. In most cases, that's the parent.

And here's the important part: liability insurance covers every person authorized to drive the vehicle. If you have a valid category B driving license and your parent allows you to drive their car, the policy covers you. You don't need to amend the contract. You don't pay extra. You don't need to visit a branch. The car is insured and you're an authorized driver — done.

That sounds simple, and in principle it is. But there are a few catches that people rarely talk about. First: if you cause an accident, the insurer pays from the parent's policy. And the parent pays the price — not directly, but through losing their no-claims bonus. For every 12 months without a claim, a driver earns a 5–10% discount on their premium. The maximum is 50–65% after ten or more years of claim-free driving. One at-fault accident means a deduction of 24–36 months from the claim-free period. A parent who built their bonus over ten years could be set back by three years.

One accident, years of loss

If you cause an accident and the insurer pays from your parent's policy, the parent loses 24–36 months from their claim-free period. That can mean thousands of crowns more per year. Consider whether it's worth insuring the car in your own name — even if it's more expensive initially.

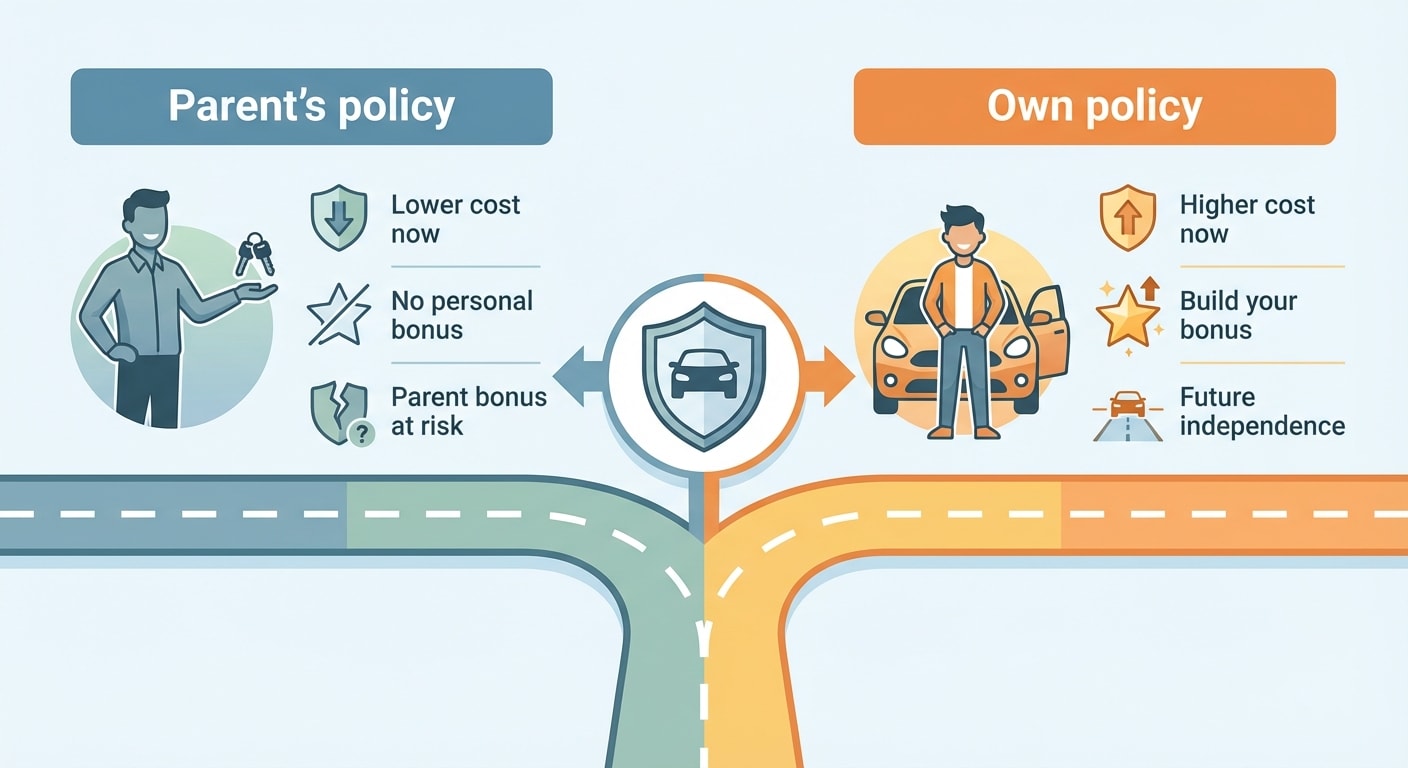

Insure under the parent, or under yourself?

This is the dilemma virtually every family with an L17 driver faces. Both options have their logic — it depends on what matters more to you: saving money now, or investing in the future.

Option 1: Car insured under the parent (most common). The parent has their bonus — say a 40% discount after eight claim-free years. The policy is significantly cheaper. You don't need to change anything. It's convenient and logical. The catch is twofold. First, if you cause an accident, the parent loses their bonus. Second — and this is more important — you don't build your own claim-free record. When you're 20 and want to insure your own car, you start from zero. No discount. Full price. And since 2020, the Czech Insurers' Bureau (ČKP) has a firm rule: no-claims bonuses cannot be transferred between family members. You can't inherit your father's bonus, even if you've been driving his car the whole time.

Option 2: Policy in your own name (investing in the future). If you're listed in the vehicle registration certificate as the operator — which is unusual for a 17-year-old, but possible — you can take out a policy in your own name. You start with no bonus, so the price will be higher. But every month without a claim builds your record. By the time you're 20, you'll have a three-year bonus and a much better position than peers who drove on their parent's policy.

Five insurers in Czechia accept 17-year-olds as policyholders: Allianz, Generali Česká pojišťovna, Kooperativa, ČSOB pojišťovna, and Pillow pojišťovna. Other insurers have no issue with L17 drivers as authorized users, but won't write an independent policy for a minor.

Generali offers a 30% L17 discount

Generali Česká pojišťovna is the first on the market to offer a 30% discount on liability insurance for L17 drivers who present proof of mentor rides before their 18th birthday. The logic is clear: a mentor reduces accident risk, and the insurer rewards it.

Watch out for the "grandpa's insurance" trick

A practice widely discussed among young drivers in Czechia: the parent (or grandparent) takes out liability insurance in their own name because they have a high no-claims bonus, and then lets the teenager actually drive the car. On paper, this is perfectly legal — the policy covers every authorized driver. But watch out for two things.

Insurers aren't naive. If they discover that the car is primarily driven by a young driver — say from a GPS log during an accident, from witness statements, or from the frequency of trips — they may charge a surcharge for a changed risk profile. In extreme cases, they may question the payout if the policyholder knowingly concealed who the main user of the vehicle is.

The second problem is long-term. The longer you drive on someone else's policy, the longer you postpone building your own bonus. And one day you'll want to insure your own car — and you'll find yourself in the same position as anyone who got their license yesterday. No discount. Full beginner's price.

It's a trade-off. You save in the short term. Long-term, it could cost you more.

How much does liability insurance cost for young drivers

Young drivers under 25 pay significantly more for liability insurance than experienced fifty-year-olds. It's not discrimination — it's statistics. Drivers under 25 cause over 10,000 accidents per year. Drivers with less than 2 years of experience make up just 3% of all drivers but cause a full 11% of accidents (BESIP 2024). Accidents involving young drivers are also roughly twice as severe as the average. Insurers know this, and the premiums reflect it.

The specific numbers depend on several factors. The most important is the driver's age — under 25, you're in the high-risk group and you'll pay more. Engine power matters too: a car with over 100 kW will drive up your premium dramatically. Your place of residence plays a role — Prague is the most expensive, small towns are the cheapest. And then there's the claim-free record, which as a beginner you simply don't have.

For reference: liability insurance for an 18-year-old driving a Škoda Fabia or Rapid ranges from roughly CZK 5,100 per year (basic limits, smaller city) to CZK 25,000 per year (higher limits, Prague, more powerful engine). An experienced driver around fifty with a full bonus pays CZK 3,000–5,000 per year for the same car. The gap is enormous — and that's the main reason it pays to start building your bonus as early as possible.

What affects your premium

Driver's age (under 25 = high-risk group), engine power (over 100 kW = dramatically more expensive), place of residence (Prague most expensive), claim-free record (beginner = 0%), vehicle type and age, chosen coverage limits. Factor all of these in when comparing quotes.

Bonus and malus — why it matters more than you think

The bonus/malus system is something most beginners don't know about — yet it affects how much you pay for insurance for the rest of your driving life.

For every 12 months with no insurance claim, you earn a bonus — a 5–10% discount on your premium. After ten or more claim-free years, you can have a discount of up to 50–65%. That's a massive difference in money. A policy costing CZK 15,000 per year with a 60% bonus costs just CZK 6,000. The claim-free record is centrally tracked by the Czech Insurers' Bureau (ČKP) — so when you switch insurers, your bonus comes with you.

Malus works the opposite way. If you cause an accident, 24–36 months are deducted from your claim-free period. If you have, say, a 12-month bonus and cause an accident, 24 months are deducted — and you're at −12. That means a surcharge on your premium, typically 10% or more. From bonus to malus in a single accident.

For L17 drivers, this is a crucial decision. If you insure under the parent, the parent keeps building their bonus (as long as you don't cause an accident), but you build nothing. If you insure in your own name, you start from zero and pay more — but in a few years you'll have your own bonus and lower premiums for life. A detailed financial comparison of both approaches is in the chapter L17 vs. Waiting Until 18, where we also break down total costs.

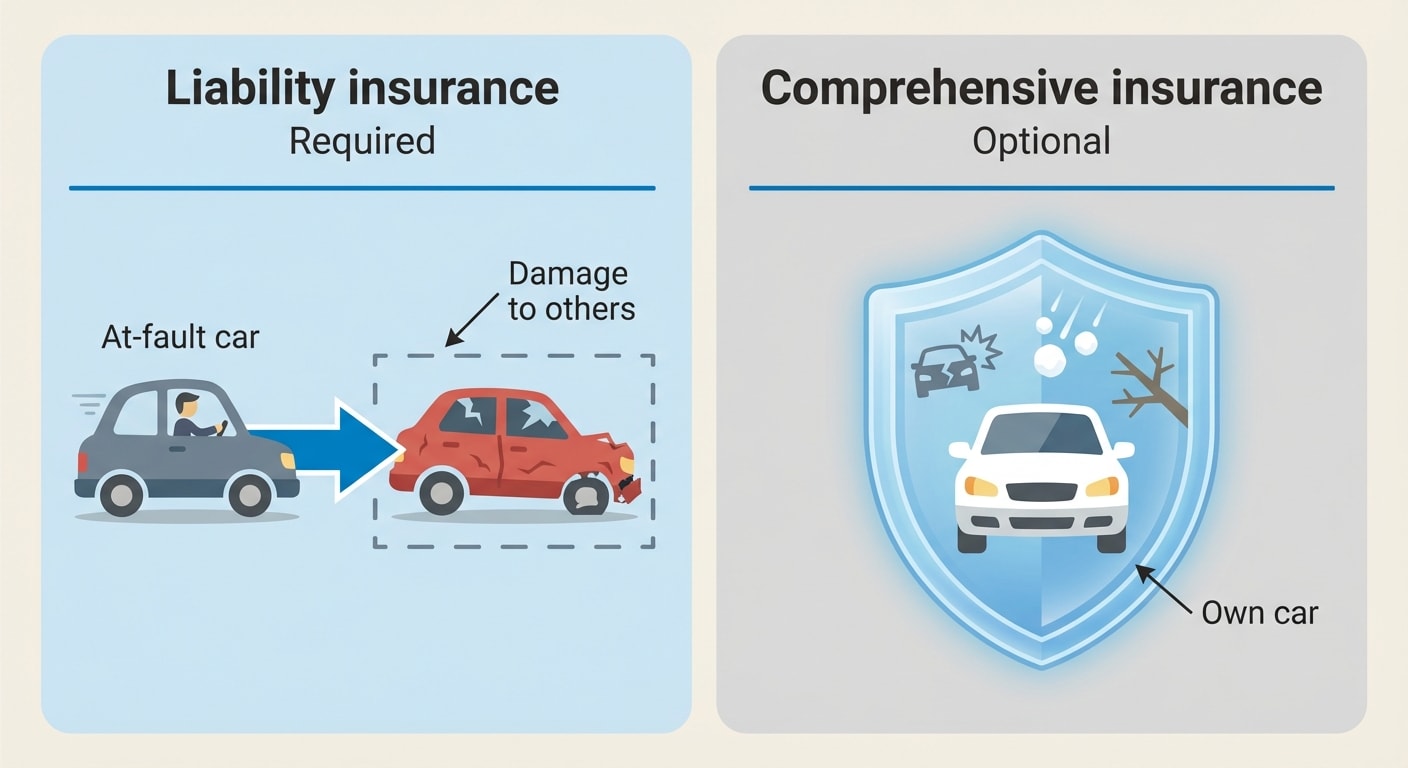

Comprehensive insurance — optional, but sensible for beginners

Liability insurance covers damage you cause to others — another car, an injured pedestrian, a damaged sign. It's required by law and without it, the car can't be on the road. But damage to your own car won't be paid from it. That's what comprehensive insurance ("kasko") is for — it's voluntary.

For beginners, comprehensive insurance makes particular sense. Inexperience behind the wheel increases the risk of damaging your own car — a scraped bumper while parking, scratching a wall in a narrow passage, a missed bollard. Nothing dramatic, but repainting modern car panels easily costs CZK 10,000–30,000. Comprehensive insurance covers these minor incidents (minus the deductible).

Most insurers don't have special L17 conditions for comprehensive insurance — they treat it as a standard contract. The price depends on the car's value, chosen deductible, and scope of coverage. The important thing to verify is whether the comprehensive policy explicitly covers L17 drivers. Usually it does, because the policy covers every authorized driver — but some contracts may have age restrictions. Ask the insurer beforehand.

What insurance to arrange and what you need for operating a vehicle is also covered in the chapter Requirements and Conditions.

What happens when an L17 driver causes an accident

This is the question parents ask most often. And the answer is unambiguous: the driver is responsible for the accident. That's you. Not the mentor. Not the parent. You.

The law (§83a of Act No. 361/2000 Coll.) states that an L17 driver is a fully authorized license holder with all rights and obligations. If you cause an accident, the police deal with you. A minor violation — say hitting a curb — is handled with a fine. A more serious accident involving injury could be classified as a criminal offence. A 17-year-old is subject to the specific provisions for sentencing minors, so penalties are milder, but the responsibility is real.

The mentor isn't off the hook either. Police examine whether the mentor fulfilled their duties — watching traffic, advising you, not being under the influence of alcohol. If the mentor neglected their supervision (for example, was sleeping or looking at their phone), they face their own sanctions. Fines for mentors for breaching their duties range from CZK 2,500 on the spot to CZK 25,000 in administrative proceedings, depending on severity. For a detailed breakdown of what mentors can and can't do, see the chapter Choosing and the Role of a Mentor.

From the insurance perspective, it works like this: the insurer pays from the vehicle operator's liability policy. If you're driving a parent's car, the parent's policy covers it. The parent loses part of their no-claims bonus. Damage to the car itself is covered by comprehensive insurance (if taken out), otherwise it comes out of pocket.

What to discuss with the insurer — practical checklist

Before you first sit behind the wheel under L17, go through this list with your parents.

First, inform the insurer that the car will also be driven by a 17-year-old driver under the L17 program. It's not a legal obligation — the policy covers every authorized driver automatically. But it's good practice and prevents problems. Some insurers appreciate the proactive approach.

Then ask whether it will affect the premium. Most insurers don't charge extra for an L17 driver if the policyholder remains the parent. But some may reassess the price if they find out the car is primarily driven by a young driver.

It's important to verify comprehensive insurance. Liability insurance covers the L17 driver automatically, but comprehensive insurance may have specific conditions. Ask whether the contract covers drivers under 18.

Finally, consider upgrading the coverage. An L17 driver is a beginner — the risk of a minor accident is higher. Higher liability limits or a lower deductible on comprehensive insurance could save a lot of money in case of an accident. Minimum statutory limits were raised to CZK 50 million in April 2024 (Act No. 30/2024 Coll.), but higher limits make sense especially for property damage.

When dealing with insurance, you might also wonder what happens to the policy once you turn 18 — we cover that in the chapter Transition to a Full License.

7 tips to save on insurance

1. Compare quotes — prices between insurers differ by thousands of crowns. 2. Buy online — there's often a discount for online purchases. 3. Pay annually — monthly installments usually cost more (installment surcharge). 4. Choose a smaller car — engine power under 100 kW = significantly cheaper policy. 5. Ask about telematics — some insurers offer up to a 40% discount for safe driving tracked via an app. 6. Bundle — liability + comprehensive together can be better value. 7. Start building your bonus as early as possible — even if the policy is more expensive at first, it pays off in a few years.

The L17 insurance paradox — safer, but not cheaper yet

The data from L17's first year is unambiguous. L17 drivers caused just 6 accidents in 2024, with zero fatalities. Drivers who got their license at 18 without a mentor caused 1,106 accidents with 6 fatalities (BESIP 2024). L17 drivers committed only 71 point-bearing offences — just 8.4% of all offences by new drivers. Similar data comes from Germany, where the BF17 program has been running since 2004: graduates have 28.5% fewer accidents (University of Gießen).

Logically, drivers with a mentor should pay less for insurance. And that's exactly what Generali Česká pojišťovna is starting to offer with its 30% discount. But the rest of the market is still waiting — insurers have only been collecting their own data since 2024 and need a statistically significant sample before changing their pricing models.

For you, this means the situation will likely improve. Once insurers have two to three years of statistics, L17 graduates could automatically receive lower rates. But for now, you pay the same as anyone else in your age bracket — unless you choose Generali.

Summary

- If you drive your parents' car, you're automatically covered by their liability insurance — no changes needed

- In an accident, the parent's policy pays out and the parent loses their no-claims bonus (24–36 months deducted from claim-free period)

- Five insurers accept 17-year-olds as policyholders: Allianz, Generali ČP, Kooperativa, ČSOB, Pillow

- Generali offers a 30% discount for documented mentor rides — the only insurer to do so

- No-claims bonuses cannot be transferred between family members (since 2020) — if you drive on a parent's policy, you don't build your own bonus

- The driver (not the mentor) is always responsible for an accident, though the mentor may be fined for neglecting supervision

Key Terms

| Term | Explanation |

|---|---|

| Liability insurance (povinné ručení) | Mandatory motor vehicle liability insurance — covers damage caused to others. Without it, the car can't be on the road. |

| Comprehensive insurance (kasko) | Voluntary insurance covering damage to your own car — scratches, accidents, natural events, theft. |

| Vehicle operator (provozovatel) | The person listed in the vehicle registration certificate as the operator — since April 2024, this is who must have liability insurance (Act No. 30/2024 Coll.). |

| Policyholder (pojistník) | The person who signed the insurance contract and pays the premiums. For L17, this is usually the parent. |

| No-claims bonus (bezeškodní průběh) | Discount for every 12 months without a claim — 5–10% per year, maximum 50–65%. Tracked centrally by ČKP. |

| Malus | Surcharge on the premium after causing an accident. One accident deducts 24–36 months from the claim-free period. |

| ČKP (Czech Insurers' Bureau) | The central institution tracking insurance contracts and claim-free records for all drivers in the Czech Republic. |

| Coverage limits (pojistné limity) | Maximum amount the insurer will pay for a single claim event. Minimum limit since April 2024: CZK 50 million. |

| Telematics | Technology tracking driving style via a mobile app. Some insurers offer up to a 40% discount for safe driving behaviour. |