Save on Car Insurance — Tips for New Drivers

Car choice, telematics, insurer comparison, family bonus. 9 strategies to save CZK 3,000–8,000 per year on new driver insurance premiums.

An 18-year-old driver in Prague pays over CZK 14,000 a year for liability insurance on a Škoda Fabia. Their parent pays just under CZK 3,300 for the same car. That's a CZK 11,000 difference. Every year. Same car, same road, same city. And yet there are at least nine ways to bring that price down by thousands — without bending any rules.

In the chapter Why Young Drivers Pay More, we explained why insurers charge new drivers two to three times more. Now comes the practical part. This article shows you specific strategies that, combined, can realistically save you CZK 3,000–8,000 a year on insurance premiums. No grey-area tricks — just smart decisions that most young drivers don't know about.

Quick summary:

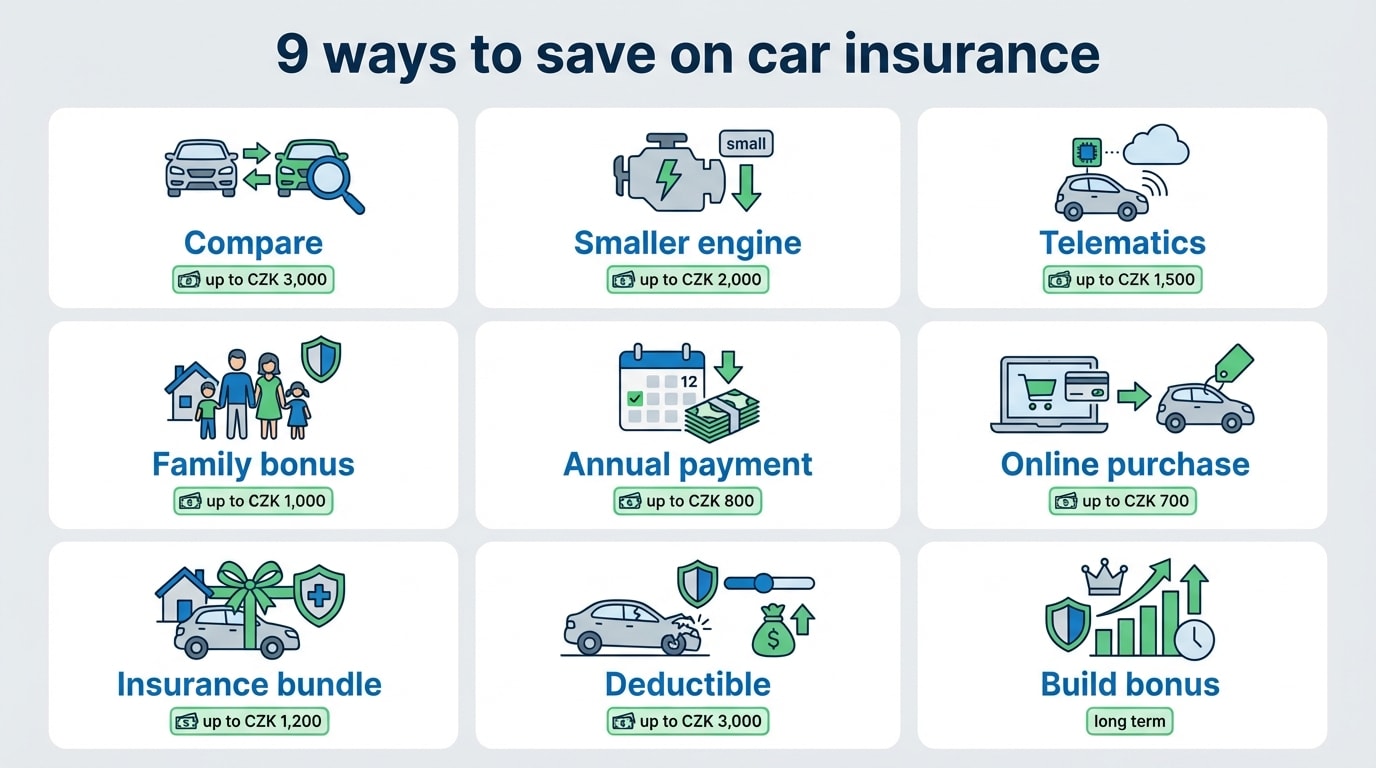

- Comparing insurers saves CZK 2,000–5,000 per year — the quickest step, takes a few minutes online

- A car with an engine under 1,200 cc and output under 75 kW costs significantly less to insure than a more powerful vehicle

- Telematics (Koopilot from Kooperativa) returns an average of CZK 3,000/year — just for driving safely

- Insuring under a parent's name works, but carries risks — in a crash, the parent loses their bonus and you don't build your own history

Compare quotes — save thousands in five minutes

Out of all strategies, this one is the simplest and fastest. Price differences between insurers for the exact same car and driver can amount to thousands of crowns per year. All it takes is filling out one form on a comparison site — and within minutes, you'll see what the market offers.

Here's the step-by-step. Go to an online comparison site — ePojisteni.cz, Srovnejto.cz, or Top-Pojisteni.cz. Enter your licence plate or manually input the car type, year, and engine size. Fill in your details: age, postcode, current claim-free period. Within seconds, the system spits out offers from dozens of insurers sorted by price.

But be careful — the cheapest offer isn't always the best. Pay attention to coverage limits. The legal minimum is CZK 50 million for both health and property, but some insurers offer higher limits for a similar price. Check what's included in the price — roadside assistance, personal injury cover, legal protection. Sometimes a cheaper policy ends up costing more because the important stuff is missing.

Among online-focused insurers, Direct (purely online, lower operational costs), ČPP (Česká podnikatelská pojišťovna), and Pillow (targeting young, digitally savvy customers) tend to perform well on price. But prices change and depend on your specific profile, so always compare.

Realistic savings: CZK 2,000–5,000/year compared to just taking the first offer that comes your way.

Compare every year

Insurer prices change every six months. You can cancel your policy at least 6 weeks before the contract anniversary. Run a new comparison every year — what was cheapest last year may not be cheapest this year.

Choose a car that won't sink your budget

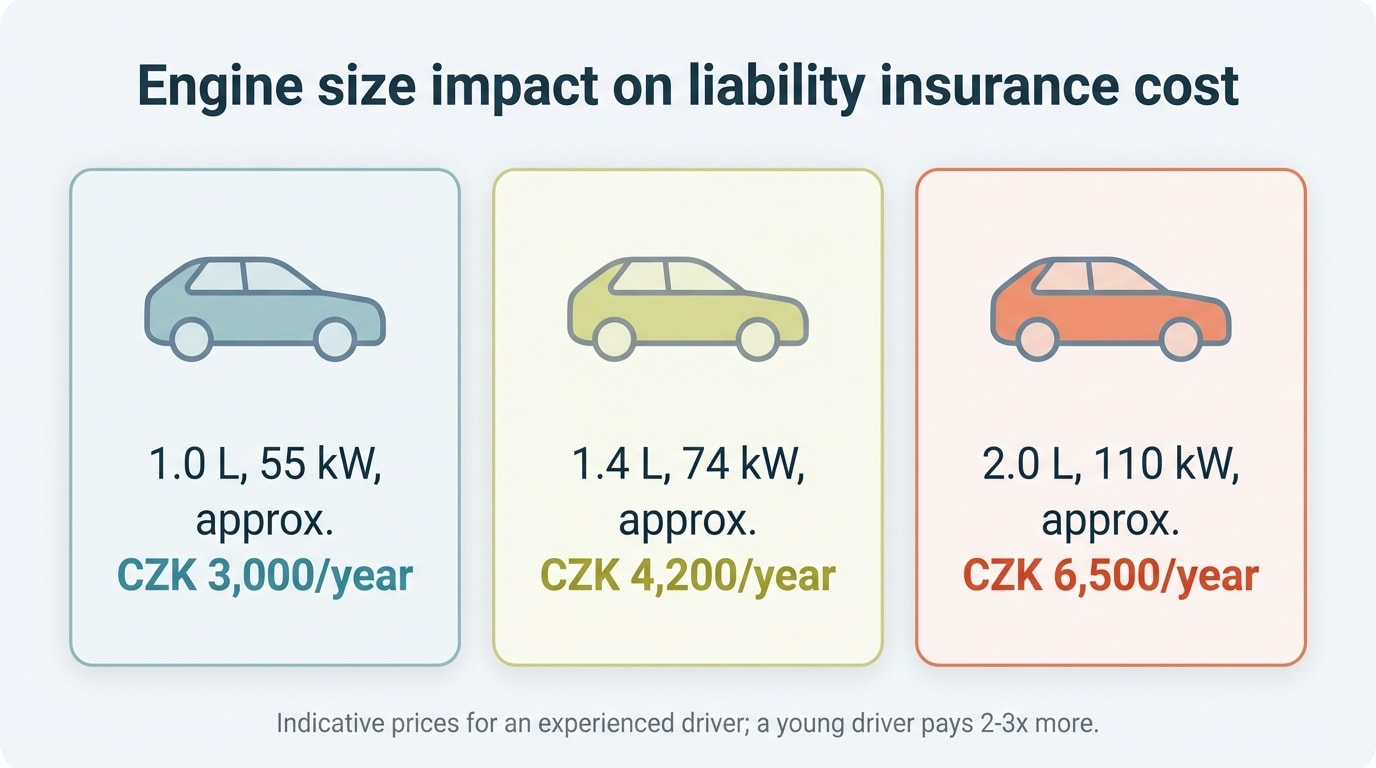

Your first car is a decision that will affect your insurance costs for years. Insurers categorise vehicles by engine displacement: up to 1,000 cc, up to 1,250 cc, up to 1,350 cc, up to 1,400 cc, up to 1,650 cc, and above. Each jump up means a more expensive policy. And not just insurance — fuel consumption, servicing costs, and road tax go up too.

The ideal first car from an insurance perspective has a petrol engine under 1,200 cc and around 55–75 kW of power. In practice, that means a Škoda Fabia, VW Polo, Toyota Yaris, Hyundai i20, or Suzuki Swift. These cars can be found as four- to eight-year-old used vehicles at a reasonable price, and you'll save CZK 1,000–3,000 per year on insurance compared to a more powerful car.

Petrol is cheaper than diesel — diesel engines carry higher insurance rates. And the car's age matters for a different reason: if you buy a car worth less than CZK 100,000, comprehensive insurance usually doesn't make sense. The annual premium would exceed what you'd get back in a total loss. For a car worth CZK 50,000–80,000, it's better to skip comprehensive coverage and set that money aside as a reserve.

On the other hand — if your car is on a lease or loan, the bank will require comprehensive insurance. In that case, go for a higher deductible (CZK 10,000–15,000) to bring the monthly premium down. More on comprehensive insurance in the dedicated chapter.

Telematics — let your driving speak for you

Telematics is the most interesting innovation on the market for young drivers right now. The principle is simple: the insurer monitors your driving style through a mobile app and gives you money back based on how you drive. Drive safely? You pay less. Drive aggressively? No discount.

The most widely used telematics product in Czechia is Kooperativa's KOOPILOT. It works as a mobile app that tracks speed, acceleration, braking, cornering, and even whether you use your phone while driving. Based on this data, it assigns you a score and pays out a cashback of 10–40% of your premium — four times a year.

In practice, the average Koopilot user gets back roughly CZK 740 per quarter, which comes to around CZK 3,000 per year. Ten percent of drivers achieve the maximum rating and get the full 40% back. That's a substantial amount, especially when a young driver's premium starts so high. One catch, though — Koopilot only works in combination with Kooperativa's "Auto komplet" comprehensive insurance. Liability-only coverage doesn't qualify.

Pillow insurance takes a different approach. They offer pay-per-kilometre insurance — you pay based on how much you actually drive. If you drive less than 12,000 km per year, this option could be worthwhile. The minimum is 5,000 km, the maximum 25,000 km. If you exceed your limit, you only pay an additional CZK 0.24 per extra kilometre — not a jump to the next full bracket. Verification is simple: you photograph your odometer two weeks before your contract anniversary.

According to a Pillow survey, 70% of Czech drivers know about pay-per-km insurance, but only 20% have used it so far. Yet over two million passenger cars in Czechia drive less than 12,000 km per year. If you're one of them — say, because you commute to school by public transport and only use the car on weekends — it's worth looking into this model.

Telematics is ideal for new drivers

You have no claim-free bonus, but you drive carefully? Telematics lets you prove to the insurer that you're a safe driver — and get rewarded for it. It's the fairest way to get around the problem of missing history.

Insurance under a parent's name — it works, but has catches

This is the most commonly used trick among young drivers in Czechia. Roughly three-quarters of young drivers register their car or policy under a parent's name, because a parent with a ten-year bonus of 50–60% pays a fraction of what a new driver without history pays. The difference can be CZK 11,000 per year or more. It's no wonder it's tempting.

But it's not risk-free. In the event of an accident, the parent loses their bonus — driving up insurance costs for the whole family. Some insurers watch for this: Slavia, for example, applies a 30% risk surcharge when the vehicle owner and main driver aren't the same person. And the main problem? You're not building your own claim-free history with ČKP (Czech Insurers' Bureau) the entire time. When you eventually want to insure a car in your own name, you'll start from zero again. The problem is only being postponed.

As for transferring a bonus within a family — most major insurers have been phasing this out since 2020. Česká pojišťovna discontinued its "Family Offer" programme in August 2020. Kooperativa doesn't transfer bonuses between relatives. Allianz and Generali allow transfers, but only between spouses. ČSOB has a "Rodinka" programme, but it's significantly restricted. Triglav and Slavia copy the bonus between spouses sharing a household.

Registering under a parent isn't illegal. But it's a trade-off — you save now, you pay later. If you're already doing it, plan to switch to your own policy within two to three years and start building your bonus. The sooner you begin, the sooner you reach a reasonable rate. More on how the bonus and malus system works in the first chapter.

Risk of registering under a parent

In an accident, the parent loses their bonus, not you. Some insurers charge a surcharge when the owner ≠ driver. And most importantly — you're not building your own claim-free history with ČKP. After 3–5 years on a parent's policy, you'll start from scratch when switching to your own contract.

Five more tricks that add up

None of the following strategies will save thousands on their own. But together they add up, and combined with insurer comparison and the right car, they can shave another few thousand crowns off your premium.

Pay annually. Insurers charge a surcharge for splitting payments into monthly or quarterly instalments — typically 5–10%. If you can afford to pay the full year upfront, you'll save hundreds of crowns with zero compromise on coverage. On a premium of CZK 8,700, that's a saving of CZK 400–870.

Buy online. Online policies tend to be cheaper than those purchased through a branch or insurance agent. The insurer saves on distribution costs and passes some of the savings to you. Sometimes it's a 5–10% discount, sometimes a small bonus or expanded coverage included in the price. And besides — online comparison sites save you time. No need to visit branches and compare offers by hand.

Bundle products with one insurer. If you take out liability and comprehensive insurance with the same company, you'll usually get a package discount of 5–15%. Some insurers also factor in life insurance or home insurance from the same provider. Ask about it — agents and online forms don't always display this automatically.

Deductible on liability? Tread carefully. Some insurers offer cheaper liability insurance with a deductible — typically 5–10% of the claim value, with a minimum of CZK 1,000–5,000. On paper, it lowers your premium. In practice, most experts advise against it. One accident and your savings go to the deductible — plus you lose months of bonus on top. For liability insurance, it's better to have clean coverage without strings attached. A deductible makes more sense with comprehensive insurance, where it's about your own car.

Build your bonus from day one. For every 12 months without an at-fault accident, your discount grows by roughly 5–10%. The maximum bonus of 60% discount is reached after approximately 10–12 years of claim-free driving. That sounds far off, but the first three years are crucial — your premium drops noticeably during that time. One at-fault accident deducts 24–36 months from your claim-free history, so drive carefully, especially at the start. Bonus data is centrally held by ČKP (Czech Insurers' Bureau) and transfers when you switch insurers. What happens to your bonus after an accident is covered in chapter five.

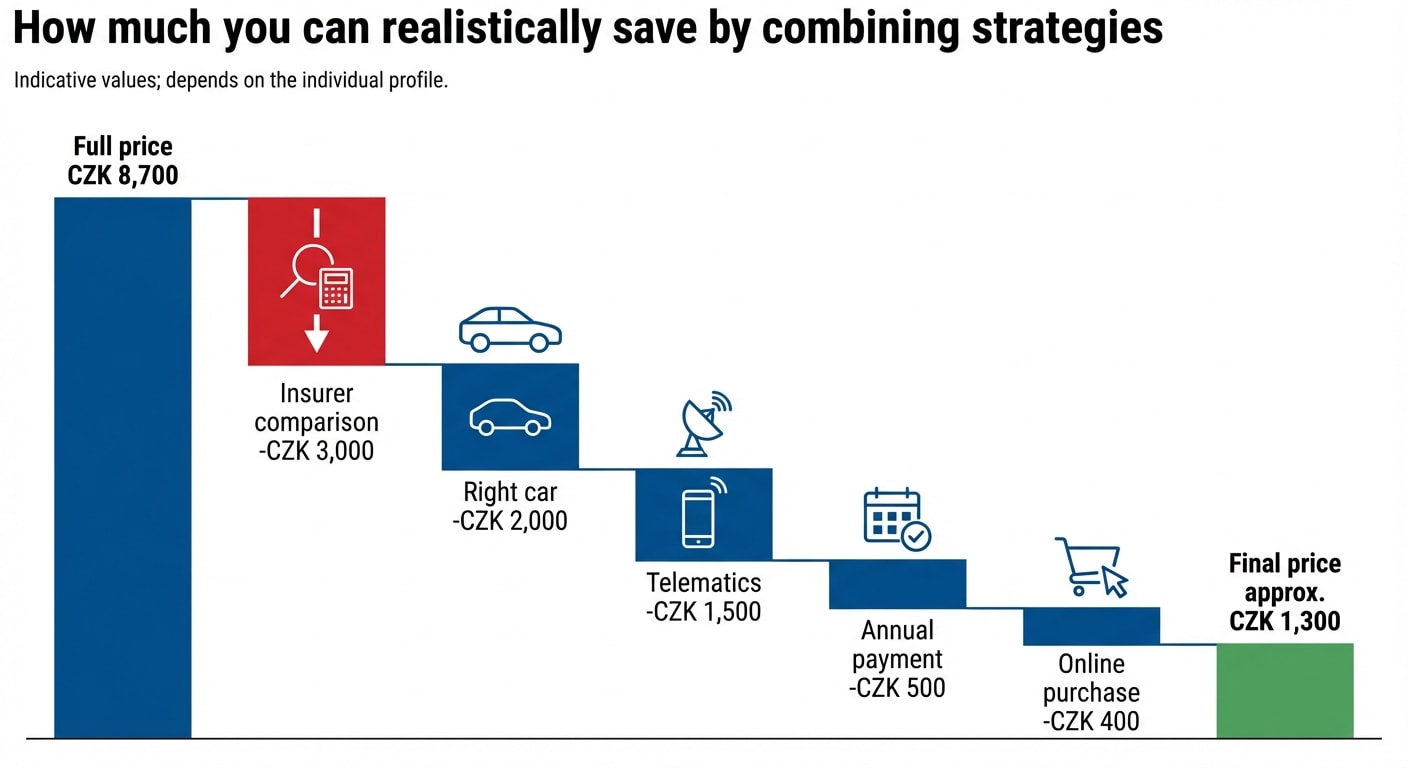

How much you'll realistically save

Let's put it all together. If you combine multiple strategies — and that's the key, no single strategy works miracles on its own — the realistic savings for a young driver range between CZK 3,000 and CZK 8,000 per year.

Comparing insurers saves you CZK 2,000–5,000 compared to the most expensive offer on the market. A smaller engine (1.0 instead of 1.6) means savings of CZK 1,000–3,000 per year. Telematics via Koopilot returns an average of CZK 3,000 per year. Online purchase and annual payment add another 5–10% off the price.

The exact figure depends on your age, car, place of residence, and specific insurer. But even the most conservative estimate — comparing quotes, buying online, and paying annually — moves you thousands of crowns lower. And if you add a sensible car choice and telematics on top, you're on your way to a premium that doesn't hurt.

Don't forget: your premium drops with every year of claim-free driving. The first few years are the most expensive. But after three to five years of careful driving, you'll be paying significantly less — and after ten years, you'll reach a level where liability insurance is just a minor annual expense. You've got this.

Example: Tomáš, 19, Škoda Fabia 1.2

After getting his licence, Tomáš bought a used Fabia for CZK 95,000. He compared insurers and took out liability insurance online for CZK 6,800/year (instead of CZK 11,500 at the most expensive provider). He pays annually, not monthly — saving another CZK 400. He doesn't have comprehensive insurance on a car worth CZK 95,000 — it wouldn't be worth it. Total savings compared to the worst-case scenario: over CZK 5,500 per year.

Summary

- Compare insurers — the quickest saving, takes a few minutes. Price differences between offers can be thousands of crowns per year.

- Choose a car with an engine under 1,200 cc — smaller engine = cheaper insurance. Petrol is cheaper than diesel.

- Try telematics — Koopilot from Kooperativa returns an average of CZK 3,000/year. Pillow offers pay-per-km pricing.

- Registering under a parent works, but you risk the parent losing their bonus and you don't build your own history. Two to three years maximum.

- Pay annually and online — save 5–10% on your premium with no compromise on coverage.

- Build your bonus from the start — after 3–5 years of claim-free driving, your premium drops noticeably. One accident sets you back 2–3 years.

- Total realistic savings: CZK 3,000–8,000 per year by combining multiple strategies.

Key Terms

| Term | Explanation |

|---|---|

| Insurance comparison site | Online tool (ePojisteni.cz, Srovnejto.cz) that compares prices and coverage from dozens of insurers in one place |

| Telematics | Technology monitoring driving style (speed, braking, acceleration) — rewards safe drivers with a discount or cashback |

| Koopilot | Kooperativa's telematics app — 10–40% cashback on premiums based on driving score, paid quarterly |

| Pay-per-km | Insurance model based on kilometres driven (offered by Pillow) — ideal for drivers under 12,000 km/year |

| Bonus/malus | Discount and surcharge system based on the driver's claim-free history at ČKP — roughly 5–10% discount per claim-free year, max 60% |

| Claim-free period | Number of months without an at-fault insurance event — tracked by ČKP, transferable between insurers |

| Deductible | Amount you pay out of pocket per claim (typically 5–10%, minimum CZK 1,000–5,000) |

| Bundling | Combining multiple insurance products with one insurer for a package discount (typically 5–15%) |

| ČKP | Czech Insurers' Bureau — centrally records the claim-free history of all drivers by personal identification number |