Motorcycle Insurance in Czechia 2026 — Save Money

Mandatory liability and comprehensive motorcycle insurance: prices, seasonal insurance, bonus/malus, fines for uninsured vehicles, and money-saving tips.

You bought your bike, rode your first kilometers, and felt that peculiar mix of adrenaline and freedom. But a month later, a letter arrives from the Czech Insurers' Bureau — you owe a daily contribution to the guarantee fund for every day your motorcycle wasn't insured. For a bike over 500 cc, that's 32 CZK per day. Over a year, it adds up to more than 11,000 CZK — and that's just the contribution, not the fine.

This article explains what insurance you need, how much it costs, and where you can realistically save money. Motorcycle insurance is surprisingly cheap — mandatory liability runs about a thousand crowns a year on average. But there are a few things you should know before signing a policy.

Quick summary:

- Mandatory liability insurance for a motorcycle costs around 1,000 CZK/year on average — significantly less than for a car

- Comprehensive insurance (voluntary) averages around 7,600 CZK/year — depends on the bike's value

- Seasonal insurance barely saves anything on liability; it pays off mainly for comprehensive coverage on expensive bikes

- Riding without insurance can result in fines up to 50,000 CZK plus daily contributions to the guarantee fund

Mandatory liability — you can't ride without it

Mandatory liability insurance isn't optional. Act No. 168/1999 Coll. states it clearly: every vehicle with a registration plate must carry third-party liability insurance. Motorcycles, scooters, mopeds, trikes, quads — no exceptions. And note: even a moped without a registration plate needs mandatory liability — it's arranged using the VIN number instead of the plate number.

What exactly does liability insurance cover? Damage you cause to others. If you crash into a car at an intersection, hit a pedestrian, or damage someone's fence, your insurer pays the compensation. Damage to your own motorcycle is not covered — you need comprehensive insurance for that.

Minimum coverage limits since 2024 are set at 50 million CZK for bodily injury and 50 million CZK for property damage. Those numbers sound huge, but in a serious accident with multiple injuries, the limit gets exhausted faster than you'd think. That's why most insurers recommend higher limits — 100/100 million CZK or even 250/250 million CZK. The surcharge for higher limits on motorcycles is minimal since the overall policy price is low.

So how much does it actually cost? The average price of mandatory liability for a motorcycle is around 1,000 CZK per year. For small scooters and mopeds under 50 cc, it's a few hundred. For powerful bikes over 500 cc, it tops out around 2,000 CZK. Compared to car liability (averaging 5,000–8,000 CZK annually), it's a fraction — motorcycles weigh less and cause less property damage in accidents.

In 2026, liability insurance prices rose by approximately 5%, but motorcycle insurance remains one of the cheapest types of mandatory coverage on the market.

What determines your liability premium

The price depends on your bike's engine displacement and power, your age (under 25 = surcharge), residence (Prague is more expensive), chosen coverage limits, and most importantly your claims-free history — the bonus for riding without incidents. Paying annually is cheaper than monthly installments.

Comprehensive insurance — protecting your bike

Mandatory liability protects others. It doesn't protect your motorcycle at all. If you want to insure your own bike — against crashes, theft, vandalism, or natural disasters — you need comprehensive insurance. It's voluntary, but in 2024, 792 motorcycles were stolen in the Czech Republic — more than 50% increase from 2023. Prague alone saw 154 thefts, roughly one-fifth of the total. If you park your bike on the street in Prague, comprehensive insurance with theft coverage stops being a luxury and becomes a smart investment.

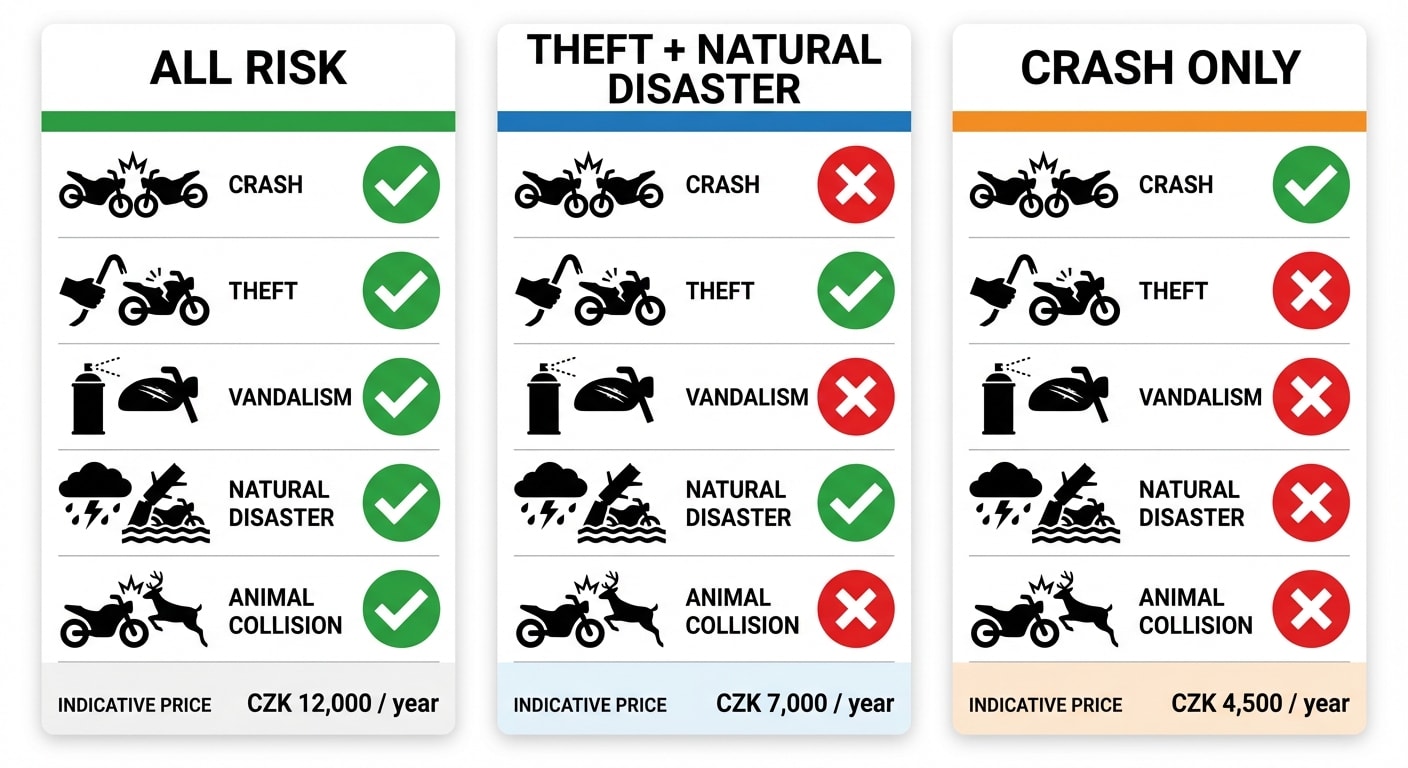

Insurers offer several comprehensive coverage tiers. All Risk covers practically everything — crash, theft, vandalism, natural disasters, and animal collisions. It's the most expensive option, but for a new or valuable bike, it makes the most sense. Theft + natural disaster is a cheaper option if you're mainly worried about theft and weather. And crash-only coverage protects against accidents — not theft or vandalism.

The average price of comprehensive motorcycle insurance is approximately 7,600 CZK per year, but the range is enormous. A scooter worth up to 40,000 CZK gets All Risk coverage for 1,300–1,500 CZK annually. A powerful bike like a BMW R 1200 RT can cost between 11,500–29,500 CZK depending on the deductible and insurer.

The key term in comprehensive insurance is the deductible. That's the amount you pay out of pocket when filing a claim. A typical deductible is 5%, minimum 5,000 CZK. A higher deductible means lower annual premiums — and vice versa. For beginners with a new bike, a lower deductible makes sense (less pain after the first drop). For experienced riders with older bikes, a higher deductible and lower payments may be the better deal.

The insurer must process a claim within 3 months of reporting and pay out within 15 days after that.

Bonus and malus — how claims-free riding rewards you

The bonus/malus system works like your "credit score" with the insurer. For every 12 months without a claim, you typically earn a 5% discount on your premium. After 10 years (120 months) of claims-free riding, you reach the maximum bonus — a 50 to 60% discount off the base price.

Conversely, if you cause an accident and the insurer pays out, the malus kicks in — a surcharge of 100 to 200% on your premium, depending on the insurer and severity of the damage. A single accident can wipe out years of bonus building.

Here's something many people don't know: motorcycle bonus cannot be transferred to a car and vice versa. They're different vehicle categories and the bonus is tracked separately. If you've been driving a car without incident for 10 years and now buy a motorcycle, you start from zero on the motorcycle policy. This fact especially surprises drivers who are expanding their license from category B — you can read about all categories and transitions in a separate chapter.

What you can do: when switching insurers, request a "Claims History Statement" from your current insurer and transfer your bonus to the new one. Free and straightforward. You can check your current bonus status by contacting your insurer, through online calculators, or via the Czech Insurers' Bureau system (SURI).

Start building your bonus from day one

Even on cheap liability insurance at 1,000 CZK per year, the bonus is worth building. After 10 years without a claim, you'll pay just 400–500 CZK annually. And most importantly — the bonus is yours and transferable between insurers.

Seasonal insurance — worth it or not?

In Czechia, motorcycles typically sit in the garage from November to March. Why pay for insurance all year when you only ride seven months? At first glance, seasonal insurance makes perfect sense. The reality is more nuanced.

Seasonal insurance works like this: the contract runs all year, but full coverage applies only during selected months — typically April through October. During the off-season, the motorcycle must be parked off public roads (garage, garden, enclosed yard). Some insurers provide off-season coverage for theft, vandalism, and natural disasters; others cover nothing.

In Czechia, seasonal insurance is offered by Kooperativa with a fixed season from April 1 to October 31, ČPP with a flexible choice of 3 to 10 months, and Allianz with monthly payment options.

Now for the key question: how much do you actually save? For mandatory liability, the savings are laughable. A full-year policy costs around 1,000 CZK; the seasonal version runs 800–950 CZK. You save a few hundred crowns per year — and in some cases, the seasonal option paradoxically costs more than the annual one. The reason is simple: insurers calculate risk, not calendar months. A motorcycle in season rides more intensively, so the risk is nearly the same.

For comprehensive insurance, the picture changes. If you have a more expensive bike with comprehensive coverage costing 15,000–25,000 CZK annually, the seasonal option can save you thousands of crowns. That's where the math starts working.

The big practical advantage of seasonal insurance: you don't have to deregister the motorcycle, return the plates, or cancel the contract — it automatically continues the next year. The downside? If a warm February weekend tempts you onto the road, you have zero coverage. And if you crash, the insurer pays nothing.

Watch out for 'off-season' riding

With seasonal insurance, you cannot ride outside the season — not even a short trip. The motorcycle must stay off public roads. If the police stop you in February with a policy valid only from April, it's the same as having no insurance at all.

What happens when you don't have insurance

Riding without mandatory liability insurance isn't just an offense — it's a financial trap that can cost you far more than a year's premium.

Police can fine you on the spot 1,500 to 3,000 CZK. In administrative proceedings, the fine can reach up to 50,000 CZK. But that's just the beginning.

The Czech Insurers' Bureau (ČKP) tracks every registered vehicle and checks whether it has valid insurance. If they find your motorcycle uninsured, they'll send you a demand for daily contributions to the guarantee fund for every uninsured day. The daily rates from 2026 (Decree No. 458/2025 Coll.) are graduated by engine displacement:

Daily contribution to ČKP guarantee fund (2026)

| Engine displacement | Daily rate | Annual cost |

|---|---|---|

| Up to 50 cc | 6 CZK | 2,190 CZK |

| 50–350 cc | 13 CZK | 4,745 CZK |

| 350–500 cc | 26 CZK | 9,490 CZK |

| Over 500 cc | 32 CZK | 11,680 CZK |

Compare: mandatory liability for a powerful motorcycle costs around 2,000 CZK per year. The guarantee fund contribution for the same uninsured bike is 11,680 CZK per year. Six times more — and that's before the fine.

The worst-case scenario: if you cause an accident without insurance, the ČKP pays the victim and then recovers the full amount from you. This recourse claim can reach up to 300,000 CZK. In a serious accident with severe injuries, it can be even more. That thousand crowns for liability insurance suddenly looks like the best investment of the year.

Supplementary coverage — what else to consider

Beyond mandatory liability and comprehensive insurance, insurers offer a range of add-ons that may make sense in specific situations.

Passenger accident insurance covers you and your pillion rider in case of injury during a crash. Given that motorcyclists have a 26× higher probability of death in an accident compared to car occupants, this policy isn't paranoia.

Roadside assistance includes towing, on-site repair, alternative transportation, and sometimes accommodation. If you plan longer rides or travel across Europe, you'll appreciate assistance services — towing a motorcycle from the Alps without coverage can cost tens of thousands.

Luggage insurance makes sense mainly for travelers carrying expensive gear in panniers.

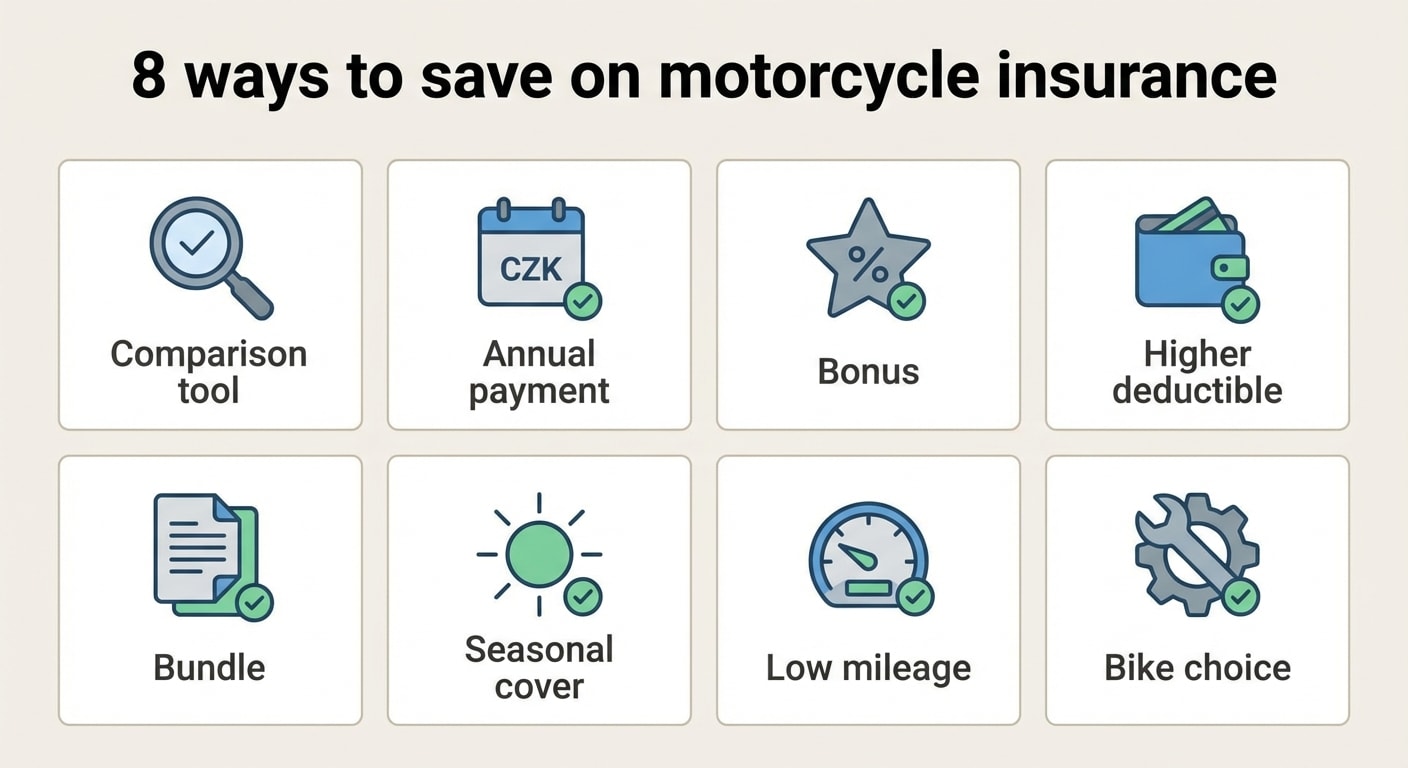

8 tips for saving on motorcycle insurance

Motorcycle insurance is already cheap, but that doesn't mean you can't pay less. Here's how.

First: compare offers. Prices between insurers differ by tens of percent. Use comparison tools like ePojisteni.cz or Srovnejto.cz — fill out one form and within a minute you have an overview of quotes. It's the fastest way to find out if you're overpaying.

Second: pay annually upfront. Monthly installments are convenient but more expensive. Annual payment saves you up to 15% of the total price. On comprehensive insurance at 7,600 CZK, that's over a thousand crowns.

Third: ride claim-free and build your bonus. The most powerful lever on your insurance price is your claims-free history. After 10 years, you pay roughly half. When switching insurers, transfer your bonus via a "Claims History Statement."

Fourth: choose a higher deductible on comprehensive insurance. If you can afford to pay the first 10,000 CZK yourself, the premium drops significantly. On an older bike with lower value, this makes particular sense.

Fifth: bundle with one insurer. Combining liability and comprehensive coverage with the same insurer earns you a package discount.

Sixth: consider seasonal insurance only for comprehensive coverage. As we showed, it barely saves on liability. For pricier comprehensive insurance, however, the savings can be in the thousands.

Seventh: report low mileage. Some insurers offer discounts for fewer annual kilometers. If you use the motorcycle only for weekend rides, ask about it.

Eighth: don't underestimate bike choice. Insurance cost depends on the value, power, and engine displacement of your motorcycle. This connection is why it's worth thinking about insurance already when choosing your first bike. A cheaper motorcycle with a smaller engine = cheaper premiums.

Which insurers offer motorcycle coverage

Most major insurers in the Czech market offer motorcycle insurance. Each has slightly different terms, prices, and perks. The best approach is to compare specific quotes via a comparison tool — but for orientation: Generali Česká pojišťovna and Kooperativa are the largest with the widest branch networks. Direct pojišťovna offers the advantage of canceling your policy anytime without penalties. Allianz and UNIQA have interesting seasonal programs. ČPP stands out with flexible seasonal insurance where you choose the number of months.

Prices can differ dramatically — that's why comparison is absolutely essential. Same bike, same rider, same coverage — and the gap between the cheapest and most expensive offer can be 30 or even 50 percent. A few minutes on a comparison tool can save you thousands.

Insurance as part of total ownership costs

Motorcycle insurance doesn't sound like a big expense — and compared to the cost of the license itself or the motorcycle, it truly isn't. But it's a cost you pay every year, which is why it's worth optimizing from the start.

Mandatory liability at a thousand crowns per year is the legal minimum — skipping it makes no sense, as the consequences are many times more expensive. Comprehensive insurance is an investment that pays off especially for new and more expensive bikes. And if you park in Prague, the 2024 theft statistics speak for themselves.

At Kvalty.cz, we analyze data from more than 1,000 driving schools across the country. If you're just starting your journey toward a motorcycle license, check out how the entire process works step by step.

Summary

- Mandatory liability insurance is required for every motorcycle — averaging around 1,000 CZK/year

- Comprehensive insurance protects your bike — All Risk is the most complete option (averaging 7,600 CZK/year)

- The claims-free bonus cuts your premium in half after 10 years — but note, it cannot be transferred from a car to a motorcycle

- Seasonal insurance barely saves on liability; for comprehensive coverage on expensive bikes, it does

- Riding without insurance costs many times more than the insurance itself — fines, guarantee fund contributions, and recourse claims

Key terms

| Term | Explanation |

|---|---|

| Mandatory liability (povinné ručení) | Legally required insurance covering damage you cause to others while operating your vehicle |

| Comprehensive insurance (havarijní pojištění) | Voluntary insurance covering your own motorcycle against crash, theft, vandalism, and natural disasters |

| All Risk | The most comprehensive tier of motorcycle insurance — covers crash, theft, vandalism, natural disasters, and animal collisions |

| Deductible (spoluúčast) | The amount you pay out of pocket when filing a claim — typically 5%, minimum 5,000 CZK |

| Bonus/malus | A system of discounts and surcharges based on your claims history — 5% discount for each claim-free year |

| Seasonal insurance | Coverage only during selected months (typically April–October); the bike must be off the road in the off-season |

| Guarantee fund (garanční fond ČKP) | Fund of the Czech Insurers' Bureau from which damages caused by uninsured vehicles are paid |

| Recourse claim (regresní nárok) | The right of the ČKP to recover money from an at-fault driver who had no insurance |

| Green card (zelená karta) | Proof of liability insurance — since 2024, you no longer need to carry the physical document |

| Claims History Statement | Document from your insurer confirming your claims-free history — needed when transferring your bonus |