Motorcycle Insurance — Prices and Seasonal Plans

Motorcycle liability from CZK 145/year, seasonal insurance, comprehensive coverage, and gear protection. Complete guide for riders in Czechia.

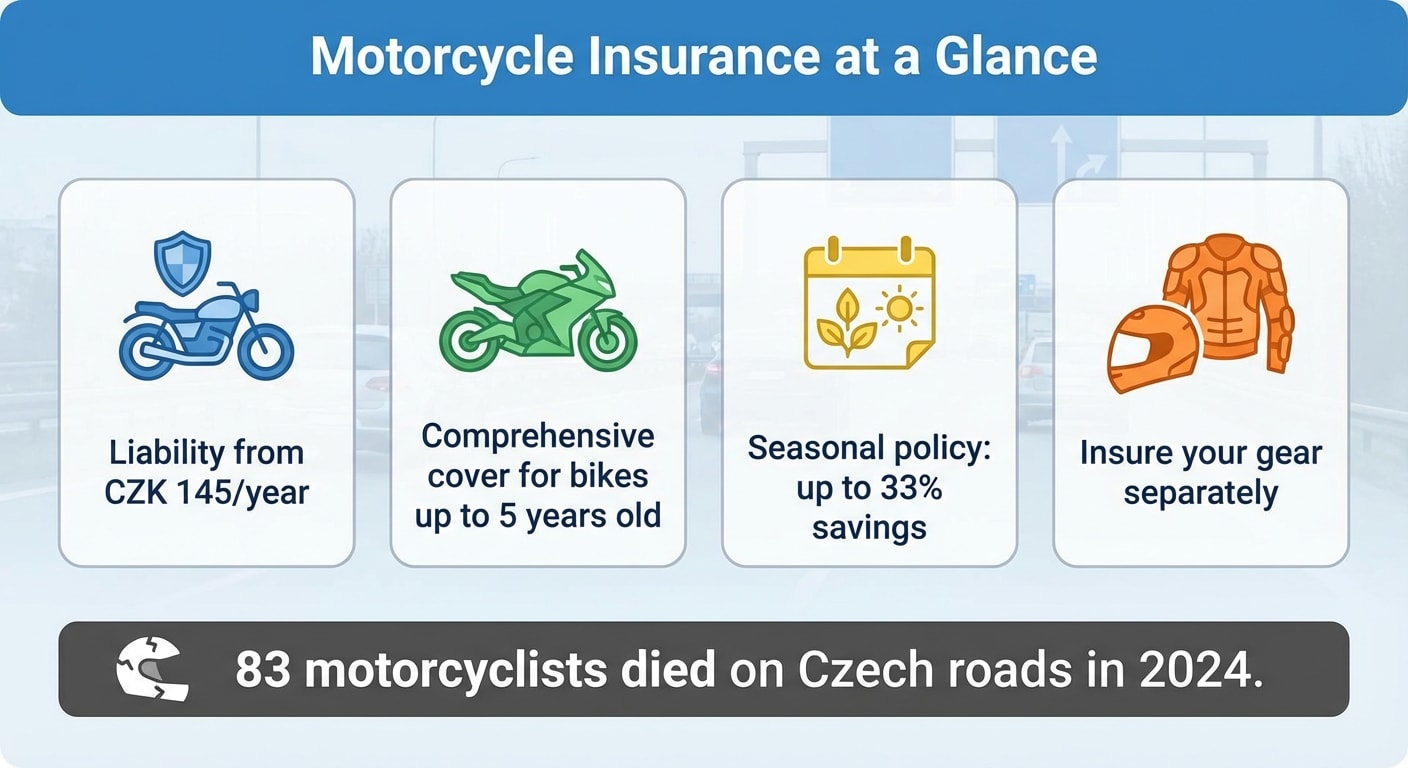

Motorcycle liability insurance starts at 145 Czech crowns per year. That's less than a cup of coffee in central Prague. And yet motorcycle insurance manages to catch riders off guard — because what works for cars doesn't apply to bikes. You can't transfer your car bonus. Seasonal insurance has pitfalls that can cost you hundreds of thousands. And gear worth tens of thousands of crowns is unprotected if someone steals it or you damage it in a crash — unless you specifically insure it.

Over 25,500 new motorcycles were registered in Czechia in 2022 — the most since 2008. But with that comes rising accident rates. In 2024, 83 motorcyclists died on Czech roads, up 12% from the year before. Czechia ranks as the 7th worst EU country for motorcyclist fatalities per million inhabitants. Proper insurance won't prevent an accident, but it can save your finances — and protect your family from debts worth millions.

Quick summary:

- Liability insurance is mandatory for every registered motorcycle — even if it sits in a garage all winter

- Prices start at CZK 145/year (under 125 cc), rising to thousands for higher-displacement bikes

- Seasonal insurance saves up to a third on comprehensive coverage — but savings on liability are minimal

- Your car bonus doesn't transfer to a motorcycle — you start from zero on a bike

Motorcycle Liability Insurance — What You Need to Know

Act No. 30/2024 is clear: every registered motor vehicle must have liability insurance. Motorcycles, mopeds, scooters, trikes, quads — no exceptions. Even that old Jawa Pioneer sitting in a garage untouched for two years. As long as it's registered, it must be insured. If you don't want to insure it, you have to deregister it.

Since April 2024, the obligation to arrange insurance shifted from the vehicle owner to the operator. In practice, this means that if a friend lends you their motorcycle, the responsibility for insurance lies with whoever is registered as the operator in the vehicle's documents.

The minimum statutory limits are CZK 50/50 million (health/property). For an ordinary bike under 250 cc, that's enough. But if you ride something more powerful, higher limits of 70/70 or 100/100 million crowns make sense. The price difference is minimal — in the order of tens of crowns per year. On a bike capable of hitting 200 km/h, it's not worth cutting corners on limits.

Small bike doesn't mean no insurance

Common misconception: 'I don't need insurance for a bike under 125 cc.' Wrong. Liability insurance is mandatory for every registered motor vehicle regardless of engine displacement. The new Act 30/2024 even extended the requirement to e-scooters over 25 km/h and off-road quads.

What Liability Costs by Engine Size

The price depends mainly on engine displacement. A small moped can be insured for a few hundred crowns a year. For a liter-class bike, you're looking at around a thousand — assuming a decent bonus. Without a bonus you'll pay more — but even then, motorcycle liability is significantly cheaper than for a passenger car.

Motorcycle Liability — Indicative Prices 2026

| Engine displacement | Lowest price | Average price |

|---|---|---|

| up to 125 cc | CZK 145/year | CZK 249/year |

| up to 250 cc | CZK 175/year | CZK 329/year |

| up to 500 cc | CZK 220/year | CZK 439/year |

| up to 750 cc | CZK 269/year | CZK 475/year |

| up to 1,000 cc | CZK 305/year | CZK 520/year |

For comparison: a Jawa Pioneer (50 cc) comes in at CZK 93 per year. A Kawasaki Ninja 650 from CZK 1,026 per year. And a Yamaha FZ6 (600 cc, 72 kW) from CZK 1,476 annually. All prices assume maximum bonus, 5,000 km per year, and 100/100 million CZK limits.

The price is driven mainly by engine displacement and power, year of manufacture, your age, residence, annual mileage, and claims-free history. Younger riders (under 25) pay a surcharge — just like with cars, age and experience are key risk factors for insurers.

Your Car Bonus Doesn't Work on a Motorcycle

This catches almost every new motorcyclist off guard. You've been driving a car for 10 years, built up a nice 50% bonus, decided to buy a motorcycle — and on the bike you start from zero. No discount whatsoever.

That's because of how the central registry at the Czech Insurers' Bureau (ČKP) works. The bonus/malus is tied to your personal ID number, but it's evaluated within 8 vehicle groups. Passenger cars and motorcycles are different groups. Your claims-free record with a Fabia doesn't count when you're arranging insurance on a Honda CB650R.

For you as a new motorcyclist, this has a concrete impact: even if you've never had an accident in a car, you start on a motorcycle without any bonus — at the base, most expensive rate. It's frustrating, but it makes sense — from an insurer's perspective, riding a motorcycle is a completely different risk than driving a car.

How to soften the blow

Formally transferring a bonus from car to motorcycle isn't possible, but some insurers offer discounts for existing clients or family members. If you have car insurance with the same company, ask about a bundle discount — it could save you 10–20% on motorcycle premiums.

General strategies for lowering your premium — choosing the right insurer, annual payment, using comparison sites — work the same as for cars. You'll find a detailed overview in the chapter How to Save on Insurance.

Comprehensive Motorcycle Insurance — More Expensive, but More Important

Liability covers damage you cause to others. It doesn't cover your bike. That's what comprehensive insurance is for — and for motorcycles it matters more than for cars, because in an accident a motorcycle is almost always heavily damaged.

Motorcycles carry higher premiums than cars. That's no coincidence — statistically they have higher accident rates and each accident causes more extensive damage. When a car scrapes against a guardrail, it needs new paint. When a motorcycle scrapes against a guardrail, you're looking at broken plastics, handlebars, levers, possibly frame damage. Repairs are expensive and quickly approach a total write-off.

Comprehensive insurance has two variants. All-risk covers collision, theft, vandalism, and natural events. Partial covers only selected combinations — typically theft plus natural events, or collision plus natural events. The most common deductible is 5%, minimum CZK 5,000. That means on a CZK 60,000 claim, you'd pay CZK 5,000 out of pocket.

Comprehensive insurance makes the most sense for newer bikes — up to 5 years old. For older machines, the residual value is lower, and the payout after deducting the deductible may not justify the annual premium. If your motorcycle is financed through a loan or lease, the bank typically requires comprehensive coverage as a condition.

When the insurer won't pay

Comprehensive insurance has exclusions. The insurer will refuse a claim if you were riding under the influence of alcohol or drugs, without a valid license, intentionally damaged the motorcycle, were racing on a public road, rode off-road (unless specifically covered), or failed to report the accident to the police when required.

Gear Insurance — What People Forget

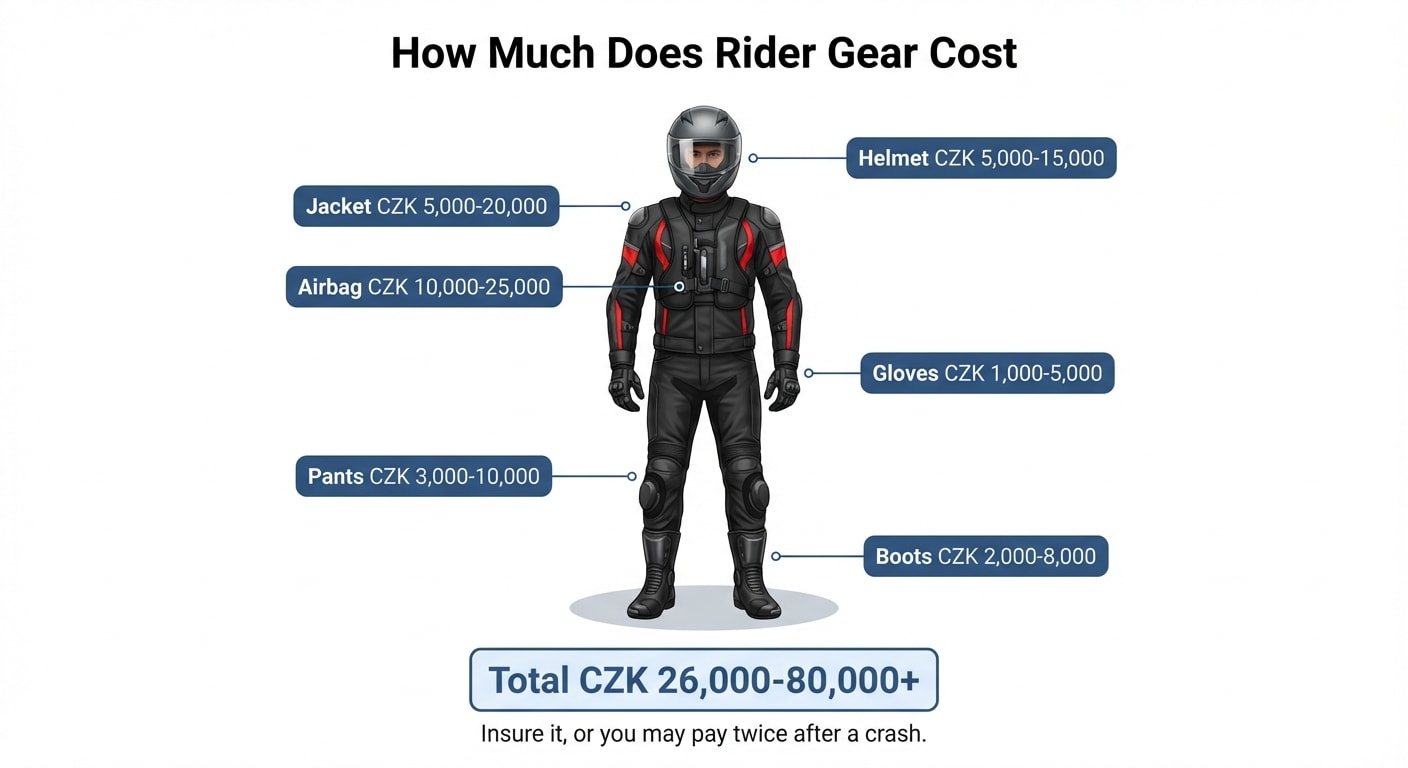

Quality motorcycle gear costs serious money. A decent helmet runs CZK 5,000 to 15,000. A jacket with armor CZK 5,000 to 20,000. Pants CZK 3,000 to 10,000. Gloves around CZK 1,000 to 5,000. Boots CZK 2,000 to 8,000. Add an airbag vest and intercom, and you can easily exceed CZK 80,000 just for gear.

Liability insurance doesn't cover gear — it only covers damage to others. Comprehensive insurance does cover gear, but only if you add its value to the motorcycle's insured amount. If your bike is worth CZK 300,000 and your gear is worth CZK 80,000, you insure the motorcycle for CZK 380,000. Then if there's an accident, damaged clothing gets reimbursed too.

An alternative is luggage insurance, offered by Generali Czech Insurance for example — with limits from CZK 10,000 to 100,000. It's a simpler option if you don't want to increase the motorcycle's insured value.

Seasonal Insurance — Is It Worth It?

Most motorcyclists ride from April to October. Why pay for insurance during months when the bike sits in a garage? That's exactly what seasonal insurance exists for.

Seasonal insurance is offered by just a handful of insurers — ČPP (Czech Entrepreneurial Insurance), Kooperativa, and a few others. Generali Czech Insurance doesn't offer a seasonal option — they argue that a motorcycle needs theft protection year-round. The minimum period is 3 months, maximum 10 months.

The savings are real: for each off-season month, you pay only about 4% of the standard price. Overall, you save up to a third compared to year-round insurance. There's also a smart combination — full coverage (collision + theft + natural events) during riding season and just theft plus vandalism in winter. This saves up to 50% compared to standard year-round comprehensive coverage.

But here's the important catch. Seasonal insurance for liability is practically pointless. Motorcycle liability costs a few hundred crowns per year. The difference between year-round and seasonal is in the order of tens of crowns — not worth the risk. Seasonal insurance pays off mainly for comprehensive coverage, where premiums are much higher.

Green card ≠ insurance coverage

Watch out for the most common misconception. The green card is a year-round document, but with seasonal insurance, coverage only applies during the contracted months. If you ride outside the season and cause an accident, the insurer won't pay — you cover the entire damage from your own pocket. The motorcycle must also be parked off public roads during the off-season (garage, private property).

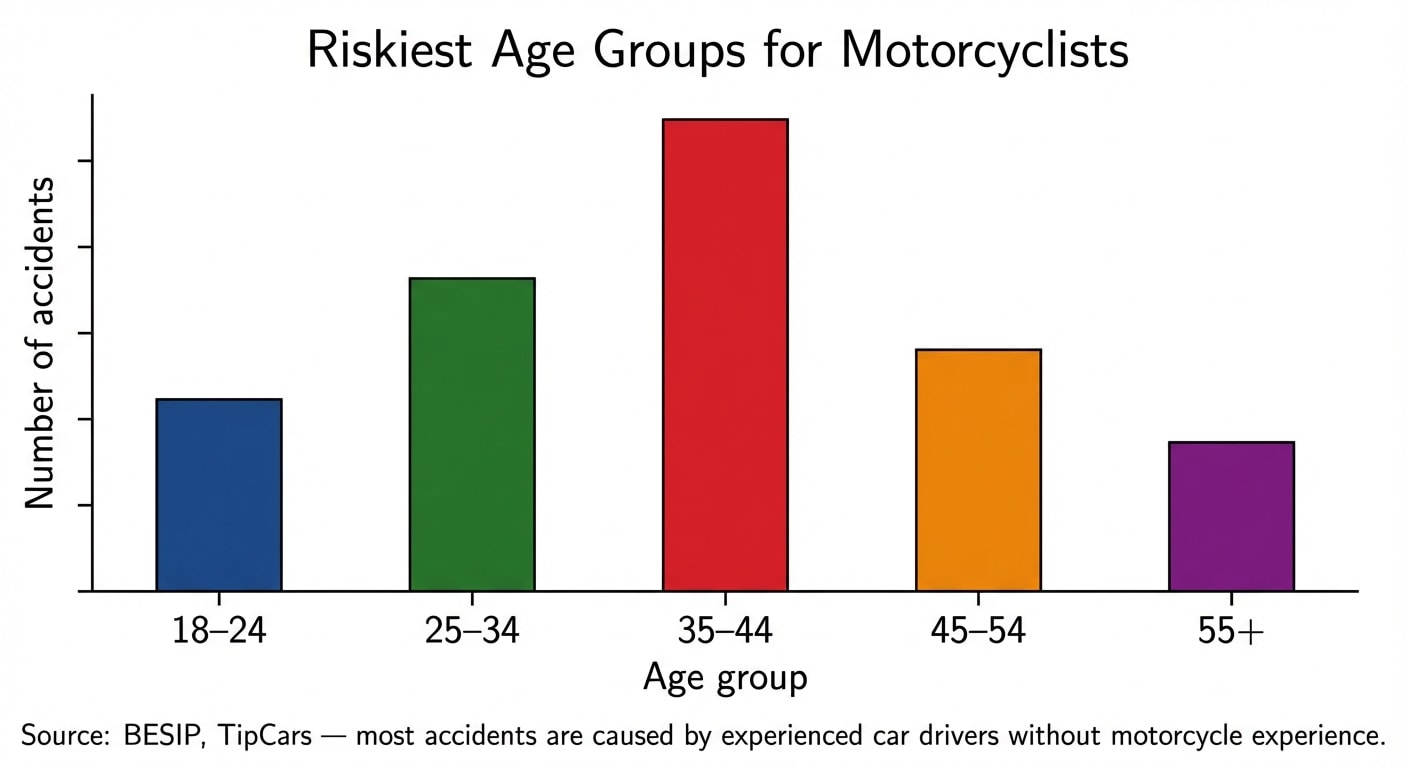

Who Crashes Most on Motorcycles

You'd expect the riskiest group of motorcyclists to be eighteen-year-old beginners? Statistics tell a different story.

The most frequent crashers are motorcyclists aged 35 to 44. People who've been driving cars for 15 years, buy themselves a lifelong dream — and discover that a motorcycle handles nothing like a car. BESIP calls this group "dads fulfilling their dreams," and the numbers are telling: 60% of motorcycle accidents are caused by the rider, 40% by car drivers. The main causes are excessive speed, failing to negotiate curves, and improper overtaking.

For you as a young rider, there's a double lesson. First: motorcycle experience doesn't automatically come from driving a car. Second: while young drivers pay higher premiums due to statistical risk, on a motorcycle age isn't the main risk factor — it's experience with that specific type of vehicle.

What Happens Without Insurance

Riding without liability insurance is an offense. Police can fine you up to CZK 5,000 on the spot. In administrative proceedings, fines range from CZK 5,000 to 40,000. But that's just the beginning.

The Czech Insurers' Bureau (ČKP) automatically monitors the vehicle registry and insurance records. For every day your motorcycle is registered without insurance, they charge a daily contribution. From 2026, it's CZK 32 per day for motorcycles over 500 cc. Annually, that comes to CZK 11,680 — plus a one-time CZK 300 fee for out-of-court collection. And the rate has been increasing — just a year ago it was CZK 25 per day.

The worst-case scenario happens if you cause an accident while uninsured. ČKP pays compensation to the injured party from the guarantee fund — and then recovers the full amount from you. Act 30/2024 removed the previous cap of CZK 300,000. Today, ČKP can charge you the full amount of the damage. In a serious accident involving a badly injured pedestrian, that means millions of crowns. The full procedure after an accident — whether you're insured or not — is covered in the chapter What to Do After an Accident.

How to Insure a Motorcycle Step by Step

The whole process is simpler than you might think. The first step is figuring out which license category you need for your motorcycle — AM (moped up to 50 cc), A1 (up to 125 cc), A2 (up to 35 kW), or A (unrestricted). This also determines the insurance price category.

You can arrange liability insurance online in a few minutes. Use a comparison site — ePojisteni.cz, Klik.cz, RIXO.cz, or Kalkulator.cz. Enter the motorcycle type, displacement, power, year of manufacture, your personal ID number, and address. The comparison tool shows you offers from a dozen insurers — Allianz, Generali ČP, ČPP, ČSOB, Direct, Kooperativa, Slavia, UNIQA, Pillow, VZP, and others.

Then consider comprehensive insurance. For a new motorcycle up to 5 years old, it makes sense. For an older one, at least consider theft coverage — motorcycles get stolen far more often than cars. Don't forget to add your gear's value to the insured amount. And if you only ride in season, ask about seasonal comprehensive coverage.

It's also worth adding supplementary coverage to your motorcycle insurance: 24/7 roadside assistance (towing, fuel, keys), rider accident insurance, and luggage insurance. Roadside assistance is especially useful for motorcycles — a flat tire on a mountain road and you're stuck without a tow.

Insure online = save money

Most insurers offer a 5–10% online discount compared to branch offices. For motorcycles where premiums are already low, it's not a huge amount — but for comprehensive insurance on a more powerful bike, online arrangement can save hundreds of crowns per year.

Summary

- Liability insurance is mandatory for every registered motorcycle — from mopeds to liter-class superbikes, even if it sits in a garage

- Liability prices start at CZK 145/year and are significantly lower than for cars

- Your car bonus doesn't transfer to a motorcycle — you start without any discount on a bike

- Comprehensive insurance costs more for motorcycles than cars, but it's worth it for newer machines

- Seasonal insurance saves up to a third — but only makes sense for comprehensive coverage, not liability

- Gear (helmet, clothing, airbag) must be insured separately — it's not covered automatically

- Without insurance, you risk fines, daily ČKP contributions, and in case of an accident, debts worth millions

Key Terms

| Term | Explanation |

|---|---|

| Liability insurance (povinné ručení) | Mandatory vehicle liability insurance — covers damage you cause to others. Applies to motorcycles the same as cars. |

| Comprehensive insurance (havarijní pojištění) | Voluntary insurance covering damage to your own motorcycle (collision, theft, vandalism, natural events). |

| Seasonal insurance | Insurance valid only for selected months of the year — typically April through October. The motorcycle must be parked off-road during the off-season. |

| Bonus/malus | Discount and surcharge system based on claims-free history. For motorcycles, it's evaluated separately from cars — it's a different vehicle category. |

| Deductible (spoluúčast) | The amount you pay out of pocket when making a claim. For motorcycles typically 5%, minimum CZK 5,000. |

| ČKP (Czech Insurers' Bureau) | Manages the guarantee fund, central insurance registry, and collects contributions from uninsured vehicle operators. |

| Green card | International insurance certificate. In Czechia replaced by online verification since October 2024, but still valid abroad as proof of insurance. |

| All-risk | The broadest comprehensive insurance variant — covers collision, theft, vandalism, and natural events all at once. |

| Gear insurance | Additional coverage for helmet, clothing, and rider equipment. Either added to the motorcycle's insured value or arranged as separate luggage insurance. |